Yes, you can travel (almost) for free. No, it’s not a scam. Yes, lots of people are doing it (including me). And yes, you can too. Here’s how it works:

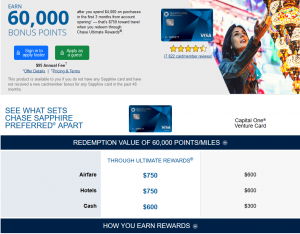

For example,* if you sign up for the popular Chase Sapphire Preferred credit card and spend $4,000 on it in three months, Chase will give you 60,000 Chase points, which can in turn be transferred to a variety of airlines and hotels.

How about London? Virgin Atlantic — another Chase partner — will fly you across the pond and back for between 20,000 and 45,000 miles, depending on when you travel and where you start.

You can even fly all the way to New Zealand for only 40,000 United miles. (But you’ll need another 40,000 to get back.)

[These numbers were correct when this summary was written, but they change often.]

[These numbers were correct when this summary was written, but they change often.]